Required Minimum Distributions (RMDs)

Turning 73? Happy birthday! Let’s talk required minimum distributions

Saving for retirement through vehicles such as 401(k)s or 403(b)s is a wise financial move, providing a secure nest egg for your golden years while offering tax benefits along the way. However, there’s one aspect of these accounts that can catch retirees off guard: Required Minimum Distributions (RMDs).

What is the rationale by this requirement?

Put simply: taxes. The tax perks associated with certain retirement accounts serve to encourage individuals to save for their golden years. These benefits often come in the form of tax deferrals, where contributions to the plan are deductible upfront but become taxable upon withdrawal. Congress was wary that these accounts could become a loophole for perpetual tax evasion if funds were left to accumulate indefinitely. Enter the RMD rules, designed to ensure that a portion of these funds is withdrawn annually.

Quick Facts

- RMDs (Required Minimum Distributions) kick in at age 73 for retirement accounts.

- RMDs apply to various pre-tax retirement plans, including 401(k)s, 403(b)s, traditional IRAs, SEP IRAs, and more.

- Failure to meet RMD requirements can result in hefty penalties, but recent legislative changes offer potential relief options for those who rectify oversights promptly.

Who needs to receive RMDs?

Starting 2024, taxpayers aged 73 and up fall under the RMD umbrella. However, nuances arise depending on whether the retirement account is an IRA or an employer-sponsored plan.

IRAs

It’s pretty straightforward here. Anyone hitting the ripe age of 73 with an IRA must take an RMD.

Employer-sponsored retirement plans

Here’s where it gets a bit more intricate. The RMD obligation hinges on whether the individual is a company owner and their current employment status.

- Ownership: If you own more than 5% of the company sponsoring the plan when you turn 73, RMDs are a must, regardless of whether you’re still on the payroll.

- Employment Status: For non-owners and those with a 5% or less stake in the company, the RMD clock starts ticking either when they hit 73 or when they bid adieu to employment, whichever comes later. However, a non-owner aged 73 doesn’t have to commence RMDs as long as they’re still actively clocking in for the employer.

It’s worth noting that if a participant aged 73 passes away, their beneficiary might have to start taking RMDs, even if they haven’t hit 73 yet.

Which retirement plans are subject to RMD rules?

RMD rules typically apply to pre-tax retirement accounts where you received a tax deduction for your contributions.

- 401(k)s

- 403(b)s

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- and more

What is the deadline for taking the RMD each year?

RMDs are due by December 31 of each year; however, for the year a participant first turns age 73, the initial RMD deadline is not until April 1st of the following year. For example, a participant who reaches age 73 in 2024 has until April 1, 2025 to take his or her first RMD, with each subsequent RMD paid by December 31 of each year.

It is important to note that that same participant is also required to take an RMD for 2025 no later than December 31, 2025. That means he or she ends up taking two RMDs in the same year and then a single RMD in each year thereafter.

You're 73 or older and still in the workforce. Can you skip taking RMDs?

Here’s the scoop: Even if you’ve hit that age threshold, you’re in luck! If you’re still employed by the organization that sponsors your retirement plan, whether full-time or part-time, you can delay RMDs from that plan.

But what if you’re a business owner with at least a 5% stake in the company? Well, for you, RMDs must kick in by April 1 of the year following the year you turn 73, regardless of your employment status.

Is RMD required from 401(k) or 403(b) designated Roth accounts?

Thanks to SECURE 2.0 Act, for 2024 and later years, RMDs will no longer be required from designated Roth after-tax accounts.

How do you crunch those RMD numbers?

Well, it’s actually pretty straightforward! The IRS has got us covered with a nifty tool called the Uniform Lifetime Table, complete with life expectancy factors. Here’s the scoop: Take your account balance from December 31st of the previous year and divide it by the life expectancy factor. That gives you the minimum distribution payment for the year. And hey, if number crunching isn’t your thing, no worries! Your retirement plan service provider, like NESA, can lend a helping hand with the calculations.

Are RMDs taxable?

Yes, RMDs are considered ordinary income by the IRS. This means they’re subject to federal income tax at your individual tax rate, as well as potentially facing state and local taxes. You’ll receive a Form 1099-R tax form detailing these withdrawals.

It’s worth noting that while RMDs are taxable, the 10% early withdrawal penalty typically doesn’t apply since recipients are over the age of 59½.

Can RMDs be taken from one account instead of separately from each account?

The approach to RMDs depends on the type of retirement plan. For example, RMDs from 401(k) and 403(b) plans must be taken separately from each account. However, IRA owners can calculate the total RMD amount and withdraw it from one or more IRAs.

Can RMD withdrawals be rolled over?

No, RMDs aren’t eligible for rollover, so it’s essential to plan accordingly for these mandatory distributions.

What happens if you fail to take annual RMDs?

Failing to withdraw the full RMD amount by the deadline can result in significant penalties. The IRS typically imposes a 50% excise tax on the amount not withdrawn. However, recent legislative changes under the SECURE 2.0 Act may offer relief, potentially reducing the excise tax rate to 25% or even 10% if the oversight is corrected within two years.

More about the age 73 requirement

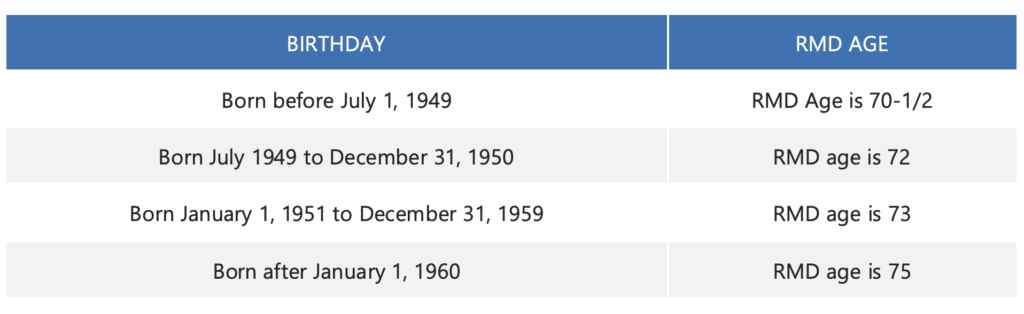

In December 2022, the SECURE 2.0 Act further increased the required age for RMDs to 73 if you turn 73 between 2023 and 2032. The age is scheduled to climb to 75 in 2033, making it a moving target.

The following table helps clarify when you’ll be required to take RMDs from your retirement accounts:

How NESA Plan Consultants can help

- Determine if you need to take RMDs

- Help calculate your RMDs

- Work with the vendor/recordkeeper to ensure your RMDs are taken out timely

Find the Right Plan for Your Business or Nonprofit

NESA Plan Consultants (NESA) is a retirement plan provider working with advisors, recordkeepers and CPAs to offer customized 401(k), 403(b) and 457(b) plans. NESA offers modern solutions and provides resources to employers and employees to secure a brighter financial future.