RETIREMENT PLAN 101

ERISA Fidelity Bond vs. Fiduciary Liability Insurance

While one is optional, the other is not. We breakdown the difference.

Similar names. Very different purposes.

Many 401(k) and 403(b) plan sponsors hear these two terms and assume they’re interchangeable. They’re not. In fact, confusing them can leave a plan exposed in ways that matter.

Let’s break it down in a simple, practical way.

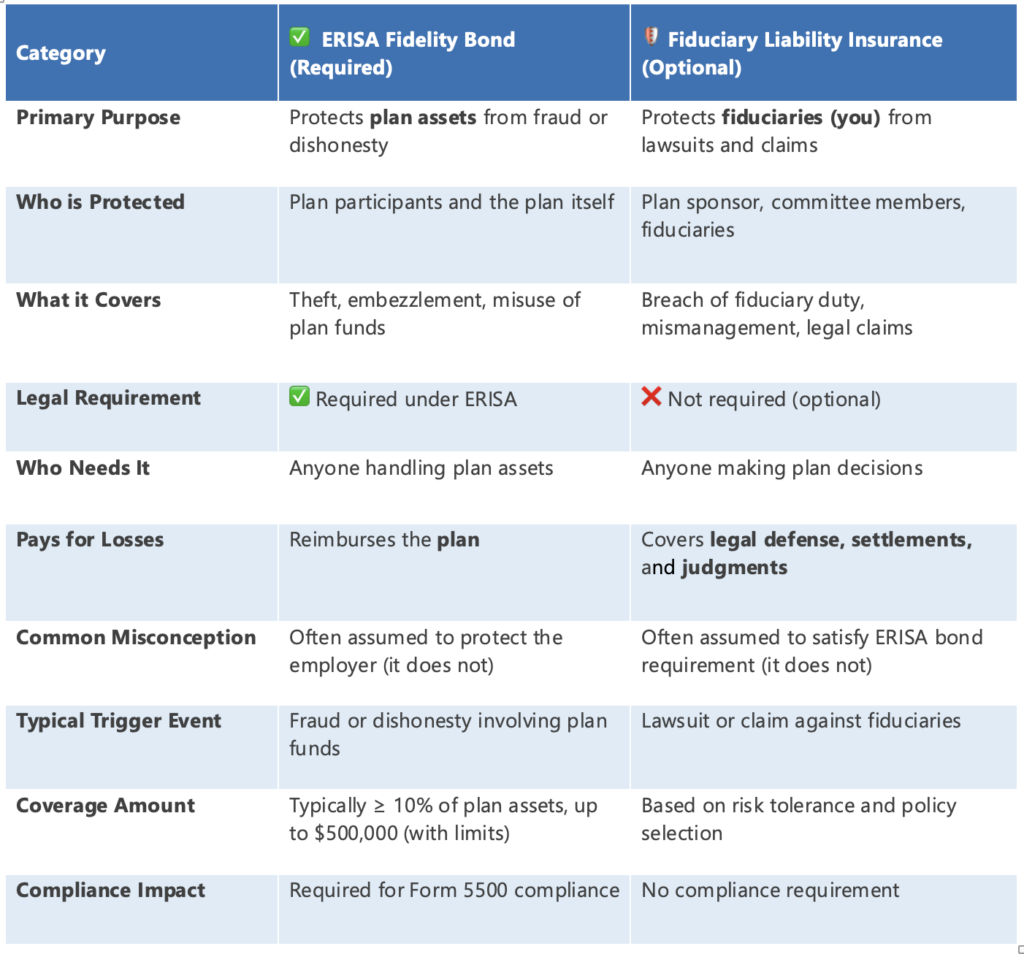

What is an ERISA Fidelity Bond? (Required)

An ERISA fidelity bond is not optional—it’s a legal requirement under ERISA for most retirement plans.

What it does:

It protects plan participants from losses caused by fraud or dishonesty (think theft, embezzlement, or misuse of plan assets).

Who it covers:

Anyone who handles plan funds or has access to them.

Key points:

• Required for most 401(k) and 403(b) plans

• Coverage typically must equal at least 10% of plan assets (with minimums and maximums)

• Protects the plan and its participants, not the employer

If your plan doesn’t have the proper bond in place, it’s considered non-compliant—something no sponsor wants to deal with during an audit or filing review.

Plan-related costs generally fall into two categories:

Quick Facts

- Required vs. Optional: ERISA fidelity bond is required by law; fiduciary liability insurance is optional.

- Who’s Protected: Bond protects the plan and participants; insurance protects fiduciaries and the company.

- What’s Covered: Bond covers fraud or theft losses; insurance covers lawsuits and fiduciary mistakes.

What is Fiduciary Liability Insurance? (Optional)

This is where many sponsors get tripped up.

Fiduciary liability insurance is not required, but it’s often a smart layer of protection.

What it does:

It protects you—the plan sponsor, committee members, and fiduciaries—from claims of mismanagement or breach of fiduciary duty.

Examples of what it may cover:

• Investment selection disputes

• Fee-related claims

• Allegations of improper plan administration

• Breach of fiduciary duty (even if alleged, not proven)

Key points:

• Completely optional

• Protects the people making decisions, not the plan assets

• Covers legal defense costs, settlements, and judgments (depending on the policy)

Why the Confusion Matters

The confusion typically comes from the assumption that having one means you’re covered for everything. That’s not the case.

Having fiduciary liability insurance does not satisfy the ERISA bonding requirement. On the flip side, having the required ERISA bond does nothing to protect the employer or fiduciaries from lawsuits or claims

One is about compliance and protecting assets. The other is about protecting decision-makers.

Where NESA Helps

This is an area where clarity matters, and it’s something we help clients navigate every day.

At NESA, we ensure that plan sponsors understand their ERISA bonding requirements and stay compliant as their plans grow. We also make the process simple by partnering with Colonial Surety Company, allowing clients to secure the required bond quickly and efficiently without added complexity.

Find the Right Plan for Your Business or Nonprofit

NESA Plan Consultants (NESA) is a retirement plan provider working with advisors, recordkeepers and CPAs to offer customized 401(k), 403(b) and 457(b) plans. NESA offers modern solutions and provides resources to employers and employees to secure a brighter financial future.