RETIREMENT PLAN 101

Front-Loading 401(k) or 403(b) Contributions: Smart Move or Missed Opportunity?

Front-loading 401(k) or 403(b) contributions can shrink the employer match if contributions aren’t spread out, but it gives your money a head start to grow through compounding.

Key Takeaways

- Front-loading means contributing the bulk of your annual 401(k) or 403(b) deferrals early in the year.

- The strategy accelerates investment growth but may reduce employer matching if no “true-up” feature exists.

- Understanding your employer’s match formula is critical before committing to this approach.

How Front-Loading Works

Front-loading contributions involves maxing out retirement plan deferrals as early as possible in the plan year. For example, instead of spreading $23,500, or $31,000 if you’re 50+ (2025 limit) evenly across 12 months, an employee might contribute heavily in the first few months, hitting the limit by spring.

This approach allows more of your money to enter the market sooner, potentially compounding for a longer period during the year. But it may lead to missed employer match.

The Pitfall of Front-Loading Contributions

The issue arises when employees aggressively defer a high percentage of their salary into their 401(k) or 403(b) at the start of the year, hitting the annual contribution limit well before December. If your employer matches contributions on a per-paycheck basis—without any adjustments for those who max out early—you’ll stop receiving matches once your personal contributions cease.

Consider this illustrative scenario based on Sansa and Jon, who both earn a $345,000 annual salary, contribute the maximum $31,000 to their 401(k) or 403(b) plans, and are paid bi-monthly (24 paychecks per year). Their employer matches 50% of the first 6% of income deferred:

- Sansa, the Front-Loader: With her $345,000 salary, Sansa defers 25% of her pay, contributing $3,593.75 per period. Her employer adds $431.25 (50% of 6% of $14,375 gross pay per period). She reaches the $31,000 contribution limit after just eight paychecks (around April), collecting only $3,450 in matches for the year.

- Jon, the Steady Contributor: Also earning $345,000 and contributing the maximum $31,000, Jon defers 8%, spreading contributions across all 24 pay periods. He hits the limit in the final paycheck and receives $431.25 per period, totaling $10,350 in matches—three times more than Sansa, despite both having the same salary and contributing the same annual amount to their 401(k) or 403(b) plans.

Although Sansa and Jon each earn $345,000 and maximize their $31,000 contributions, the timing of their contributions results in significantly different employer matches due to the per-paycheck matching system.

Not All is Lost: Why Front-Loading Can Pay Off

Markets don’t rise in a straight line, but history shows they tend to climb over the long haul. Since 1957, the S&P 500 has averaged over 10% annually. By front-loading your 401(k) or 403(b) contributions, you’re giving more of your money the chance to get in early and benefit from that potential growth. If you’re optimistic about the future, this strategy lets your savings start working harder, sooner.

Understanding Employer Matching Methods

Not all matching systems are created equal, which is why knowing your plan’s details is crucial. Employers typically use one of two approaches, with an important exception:

- Payroll Matching: The most common method, where matches are added each pay period based on that period’s contribution. No contribution means no match—putting front-loaders at risk.

- Lump Sum Matching: Contributions are matched once annually, often after year-end. Timing doesn’t matter here; as long as you contribute during the year, you get the full match

The Exception: True-Up Matching

Some employers offer a “true-up” feature. This means that at year-end, they review your total contributions and adjust their match so you receive the maximum you’re entitled to—regardless of when you contributed.

However, not all employers provide a true-up. If yours doesn’t, front-loading can cost you. Always confirm this with your HR or benefits team before deciding on a strategy.

What’s the Right Strategy for Me?

Each retirement plan works a little bit differently, so it’s critical you speak to your plan administrator and learn how the matching contribution on your 401(k) or 403(b) plan works before ultimately deciding whether or not you’d like to front-load. You may decide that a dollar-cost averaging (DCA) strategy, spreading contributions evenly like Jon, is more beneficial for your situation to maximize employer matches. You may also wish to consult a wealth planner for additional advice tailored to your financial goals.

Strategies to Maximize Your Match

If your employer sticks to basic payroll matching without true-ups, a little planning can help you avoid the trap. The key is to calculate a deferral percentage that spreads your contributions across all pay periods while still hitting the annual limit.

For example, take Barry, a 52-year-old earning $400,000 annually, eligible for a $31,000 contribution in 2025. His employer matches up to 4% without true-up:

- Divide the limit ($31,000) by salary ($400,000) to get about 7.75%.

- Set deferral to 7.75% from the start to spread evenly.

If decimals aren’t allowed, round down (e.g., to 7%) for most of the year and ramp up in the final periods. For bi-monthly pay:

- 7% for 23 periods: $1,166.67 per period × 23 = $26,833.41

- Increase to 18% for the last period to reach $31,000 total.

You could also front-load slightly by starting higher and dropping later—whatever ensures matches every period.

For those with variable income (e.g., commissions or bonuses), use a conservative salary estimate early on, then adjust in Q4. Always aim to capture the full match while maxing your contribution.

Final Thoughts

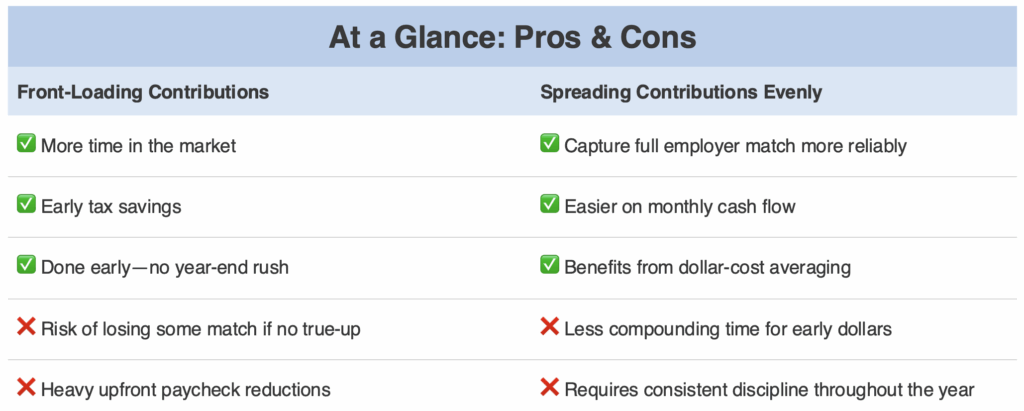

Front-loading can give investments more time to grow, potentially boosting long-term returns. However, without a true-up provision, it may also reduce the employer match. Spreading contributions evenly helps secure the full match, while front-loading offers the advantage of earlier compounding. The best strategy depends on your plan’s rules and your financial goals.

Front-Loading Contributions FAQs

Front-loading means contributing the maximum annual limit to your 401(k) or 403(b) early in the year—often within the first few months—rather than spreading contributions evenly across all paychecks.

Most employers calculate the match per paycheck. Once you’ve hit the IRS limit and stop contributing, there are no further employee contributions for your employer to match. This results in missed “free money” for the rest of the year.

A true-up provision allows employers to review your total contributions at year-end and adjust their match so you receive the full amount you’re entitled to—regardless of contribution timing. Not all employers offer this, so always confirm with HR or your plan administrator.

Yes. Even with the higher limit ($31,000 in 2025 for those 50+), the risk is the same: if your employer matches contributions per paycheck, you’ll miss out on match dollars if you stop contributing mid-year.

The safest approach is to spread contributions evenly across all paychecks unless you’ve confirmed your employer offers a true-up. This ensures you capture the full employer match while still reaching your annual contribution goal. That said, front-loading contributions can be advantageous too—your money gets invested earlier, giving it more time to grow through compounding. The best choice depends on your plan’s rules and your personal financial priorities.

This is for educational purposes only. The information provided here is intended to help you understand the general issue and does not constitute any tax, investment or legal advice. Consult your financial, tax or legal advisor regarding your own unique situation and your organization’s benefits representative for rules specific to your plan.

Find the Right Plan for Your Business or Nonprofit

NESA simplifies retirement planning by partnering with financial advisors, CPAs, recordkeepers, and industry professionals to create tailored workplace retirement solutions. From small businesses to mid-sized companies, nonprofits, and self-employed individuals, we help organizations provide meaningful retirement benefits—ensuring employees and business owners alike can save with confidence and peace of mind.