RETIREMENT PLAN 101

Understanding Catch-Up Contributions: What’s Changed and What Employers & Employees Need to Know

Catch-up contribution opportunities have expanded, but so have the rules and complexities.

What Are Catch-Up Contributions?

Catch-up contributions are additional elective deferrals that employees age 50 and older may make to their 401(k) or 403(b) plans. These contributions help individuals make up for years when they may have saved less due to family responsibilities, career changes, or other priorities.

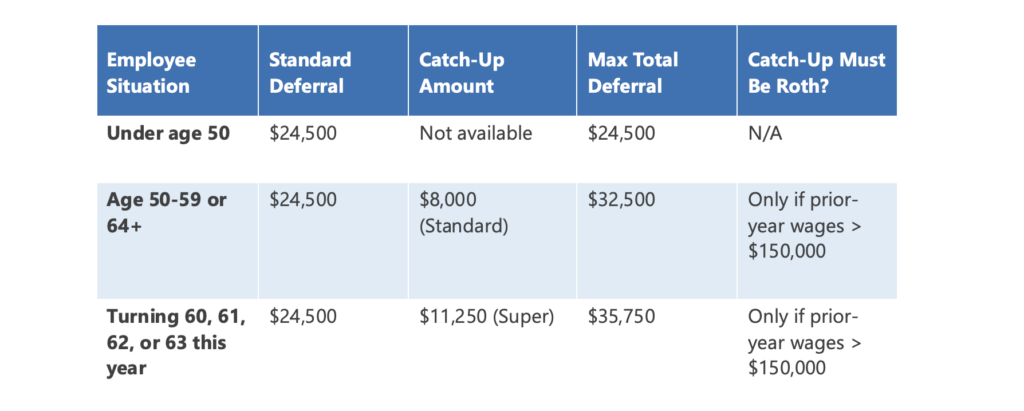

For 2026, the standard annual elective deferral limit for employees under age 50 is $24,500. Employees who are age 50 or older by December 31 of the year may contribute an additional catch-up amount on top of that limit.

Quick Facts

- Standard Catch-Up: Employees age 50+ can contribute an extra $8,000 (total deferral up to $32,500).

- Super Catch-Up: Those turning 60–63 this year can contribute an extra $11,250 (total deferral up to $35,750), if the plan allows.

- Mandatory Roth Rule: High earners (prior-year FICA wages > $150,000 from the plan sponsor) must make all catch-up contributions as Roth (after-tax).

Two Ways to Make Catch-Up Contributions

Standard Catch-Up Contributions (Ages 50+)

The classic catch-up provision has been available for many years and remains a reliable tool. In 2026, employees age 50 and older may contribute an additional $8,000 beyond the standard limit.

This brings the total employee deferral to $32,500 for those in this group (ages 50–59 and 64+). Most plans already permit this option.

Super Catch-Up Contributions (Ages 60–63)

Thanks to the SECURE 2.0 Act, a higher “super catch-up” limit became available starting in 2025 for employees who turn age 60, 61, 62, or 63 during the calendar year (provided the plan has been amended to offer it).

In 2026, this super catch-up amount is $11,250 (instead of the standard $8,000). It allows eligible employees to defer up to a total of $35,750 from their paycheck. This provision gives participants in their early 60s an extra opportunity to build momentum heading into retirement.

The Mandatory Roth Catch-Up Rule (Effective 2026)

One significant change under SECURE 2.0 took full effect in 2026: high earners must make catch-up contributions on a Roth (after-tax) basis.

If an employee is age 50 or older and earned more than $150,000 in FICA wages (reported in Box 3 of Form W-2) from the plan sponsor in the prior year, any catch-up contributions—whether the standard $8,000 or the super $11,250—must be designated as Roth contributions. Pre-tax catch-up contributions are no longer permitted for these individuals.

Important details:

- The $150,000 threshold is based solely on wages from the employer sponsoring the plan.

- Only the catch-up portion is affected. Regular contributions up to the $24,500 standard limit may still be made on a pre-tax or Roth basis (if the plan allows both).

- Employees whose prior-year wages were $150,000 or less retain flexibility to choose pre-tax or Roth for their catch-up amounts.

- The plan must offer Roth contributions for this rule to apply.

This change encourages tax-free growth in retirement and aligns with broader policy goals favoring Roth accounts.

Catch-Up Contributions at a Glance

Key notes: The above numbers are for 2026 and are subject to change. The super catch-up is available only if the plan document has been amended to include this SECURE 2.0 feature. The Roth mandate applies only to the catch-up portion. Always check plan documents and consult appropriate professionals.

What This Means for Plan Participants and Sponsors

For plan participants: Employees should review their current contribution rates, check last year’s W-2, and ask their plan administrator whether the super catch-up option is available. Those eligible for the higher limit or subject to the Roth rule can adjust their savings strategy accordingly to maximize tax-advantaged growth.

For plan sponsors and HR leaders: These updates often require plan amendments, updated participant communications, payroll system adjustments, and careful compliance steps.

Where NESA Helps

Catch-up contribution rules continue to evolve, making clarity and proactive guidance more important than ever. This is an area where NESA provides ongoing support to businesses and nonprofits and their valued employees every day.

Find the Right Plan for Your Business or Nonprofit

NESA Plan Consultants (NESA) is a retirement plan provider working with advisors, recordkeepers and CPAs to offer customized 401(k), 403(b) and 457(b) plans. NESA offers modern solutions and provides resources to employers and employees to secure a brighter financial future.