Who Pays for Retirement Plan Fees? Let’s Break It Down

In our last article, we talked about what can and cannot be paid using plan assets. Today, let’s take it one step further and talk about who ends up footing the bill—because when it comes to 401(k) or 403(b) plan costs, it’s not always the employer.

Here’s the truth: administrative, audit, and many other eligible plan-related fees can often be paid using participant accounts. And while some employers choose to cover these expenses themselves, it’s not uncommon—nor inappropriate—for the costs to be passed on to participants.

Settlor vs. Non-Settlor Expenses (Say What?)

Let’s clarify a big one: not all costs are treated equally.

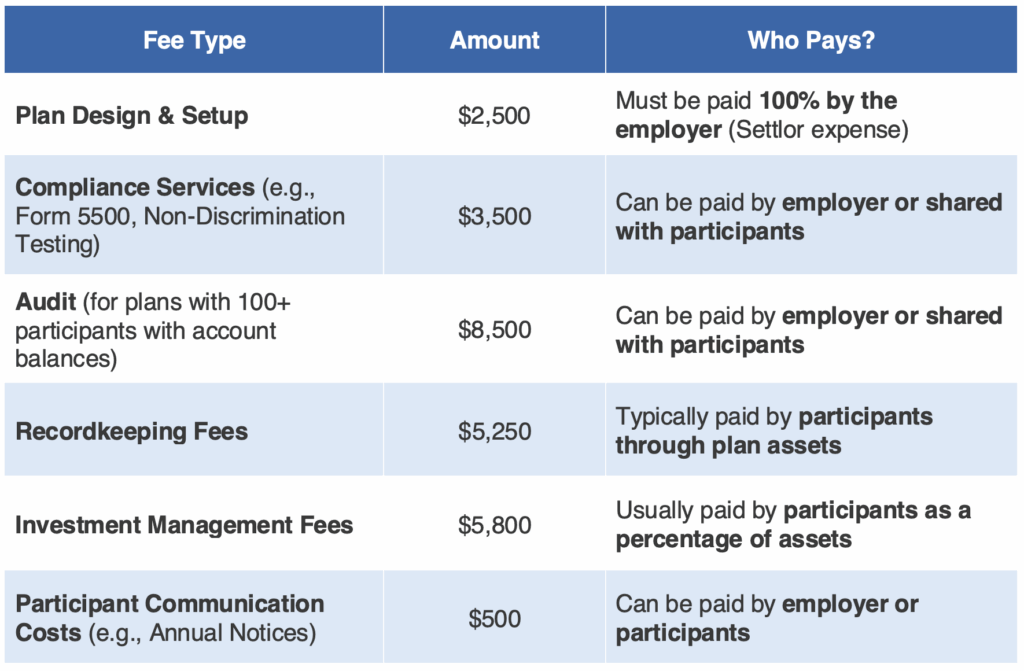

- Settlor expenses (like deciding to start a plan or choosing what kind of match to offer) must be paid by the employer.

- Non-settlor expenses (like recordkeeping, compliance testing, or annual audits) can often be paid from plan assets—meaning participants can help shoulder those costs.

But Do Employers Really Pass on the Costs?

Yes—and often in creative ways. Even if an employer doesn’t charge current employees, they may apply account fees to terminated participants with balances still in the plan. This strategy helps reduce the employer’s cost burden without affecting their active workforce.

Example: We recently worked with an organization that decided to waive fees for active employees but implemented a quarterly flat fee for terminated participants. Not only did this shift help them lower their overall expense, but it also aligned with their goal of supporting current staff while still maintaining a sustainable plan.

Fees Must Be Disclosed

Whether participants are paying a flat-dollar fee or a percentage of assets, fees must be clearly disclosed to them in advance. Transparency isn’t just a best practice—it’s required.

How NESA Helps

At NESA, we collaborate with our clients, their recordkeepers, and financial advisors to figure out what makes the most sense for their plan. Want to split fees between employer and participant? Charge only terminated employees? We help design, document, and implement those strategies.

Examples of Fee Payment Scenarios

- Participant-Paid in Full: All administrative and compliance fees come directly out of participant accounts. This can work well for employers looking to minimize plan-related expenses on their books.

- Partial Participant Payment: Employers cover a portion of the fees, while participants share the rest—often a fair compromise balancing employer budget and participant costs.

- Employer-Paid: The company absorbs all fees, providing a more “employer-sponsored” feel where employees enjoy a fee-free plan experience (at least while active).

Bottom Line

It’s totally normal for plans to have participant-paid fees. The key is understanding which fees are eligible, who’s paying them, and how they’re disclosed. And when done right, it can strike the perfect balance between employee support and business sustainability.

Need help navigating all of this? NESA’s here for it. We’ll work with your team to design a plan that fits your goals—and your budget

This is for educational purposes only. The information provided here is intended to help you understand the general issue and does not constitute any tax, investment or legal advice. Consult your financial, tax or legal advisor regarding your own unique situation and your organization’s benefits representative for rules specific to your plan.